To read the full article, click here:

Decisions, decisions: If you own a small business corporation, especially one with a calendar year-end, time is running out to optimize your ideal compensation mix of salary and/or dividends for 2010, especially if you are planning to make a 2011 contribution to a registered retirement savings plan.

That's because eligibility to make an RRSP contribution next year is based on 18% of your "earned income" this year. Earned income includes salary or bonus remuneration but does not include dividends.

But, step back for a moment and reconsider many an accountant's standard advice to business owners, which is to pay out at least enough salary to maximize your RRSP contribution.

For example, you would need to receive a salary of at least $124,722 this year to be able to contribute the maximum amount to an RRSP ($22,450) in 2011.

There are potentially two flaws with this rule of thumb, at least for Canadian-controlled private corporations with taxable income entirely eligible for the preferred corporate small business tax rate (generally $500,000 in most provinces.)

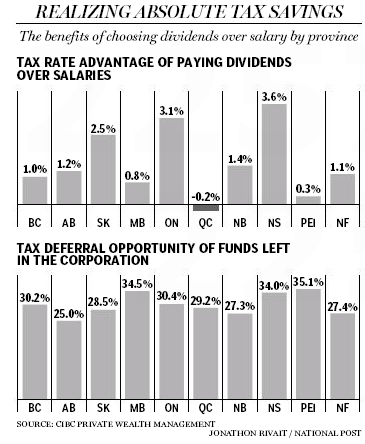

First, if you need the cash, depending on your province of residence, you may actually pay more tax on the funds withdrawn as a salary than if the same funds were taxed to the corporation and then withdrawn as dividends. I call this the "tax rate advantage" and the amount varies by provinces (see chart above).

Second, if you don't need the cash, you give up a significant tax deferral by withdrawing the funds as a salary to be taxed immediately instead of simply leaving the cash in the corporation to be taxed at a much lower small business corporate tax rate. This is known as the "tax deferral advantage" and ranges, as the chart shows, from a low of 25% in Alberta to a high of about 35% in P.E.I.

By leaving funds in the company, and investing them as you would inside an RRSP, you can build up a significantly larger investment portfolio that can later be tapped at retirement by paying out a dividend.

Other potential benefits of paying out dividends as opposed to salary are that payroll deductions, such as Canada Pension Plan contributions, Employment Insurance premiums and other provincial payroll taxes are not eligible on dividends.

For example, business owners who pay salary must contribute both the employer and employee portions of the CPP, which works out to a total of about $4,300 in 2010.

While paying enough salary to maximize CPP entitlements is often touted as one of the benefits of salary over dividends, it's questionable whether, during the course of a 40-year career, the premium savings could not be independently invested in a diversified portfolio to ultimately produce a larger pension income.

For more insight into this theory, as well as a detailed mathematical example that puts this theory into practice, you can read my full report "Rethinking RRSPs for Business Owners: Why Taking a Salary May Not Make Sense," found at cibc.com